4-Point Inspection

A four-point inspection is specifically for homeowners’ insurance and shouldn’t be confused with a new home inspection (also called a buyer’s inspection, real estate inspection, or home inspection). This distinction is important because a new home inspection is required to close on a home and meet eligibility criteria for your mortgage. It also takes two to three hours to complete.

A four-point inspection takes about 30 minutes and is only visual. However, if you buy an older home you might be required to have both inspections.

Four-point inspections identify key areas that most commonly result in insurance claims. If a home fails all or part of the inspection, the inspector will go over what needs to be fixed or replaced to alleviate deficiencies.

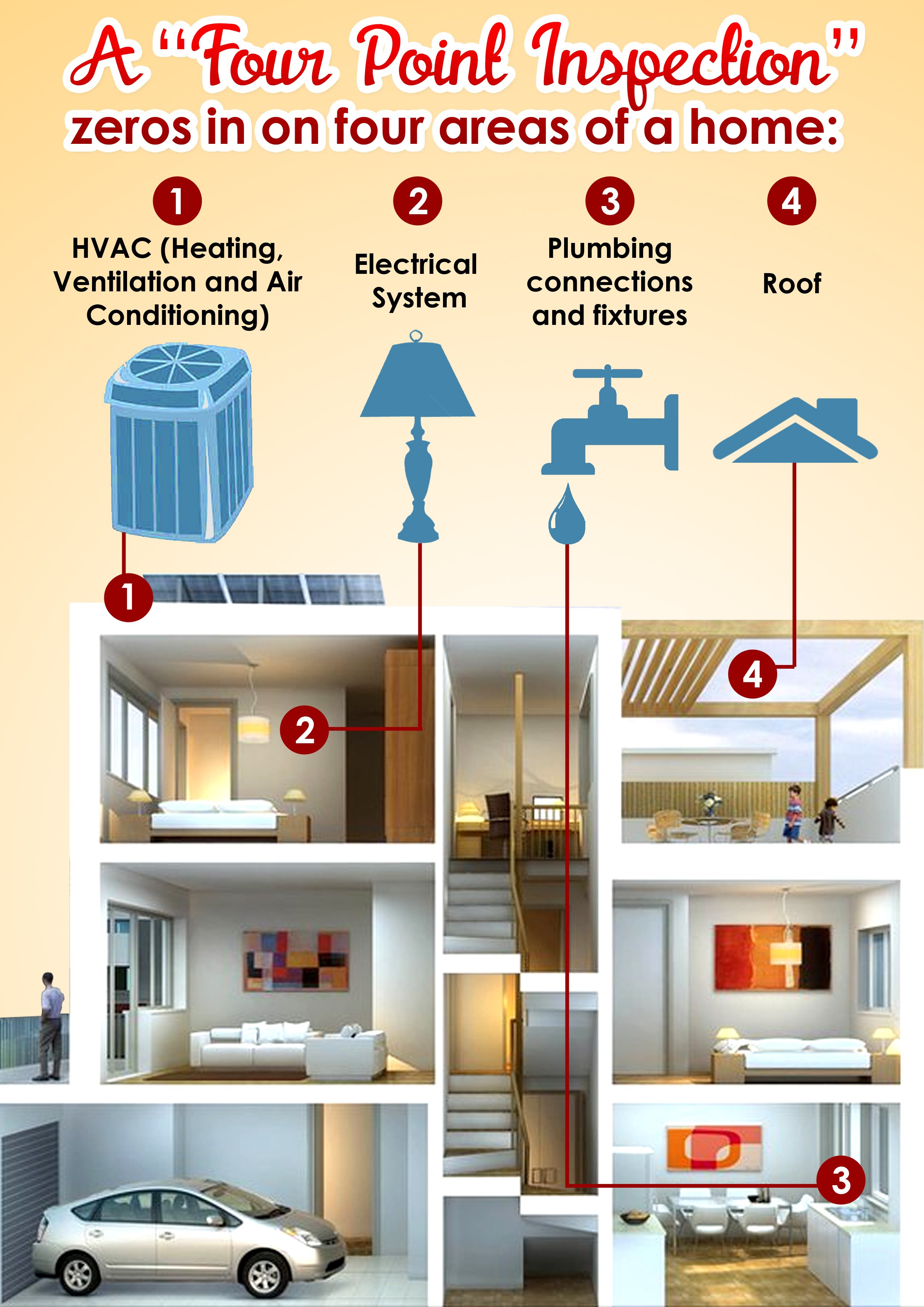

During a four-point inspection, an inspector will look at:

1) Electrical Wiring and Panels: What kind of wiring is in your home? If a home has copper, aluminum, or knob-and-tube wires, chances are it will not be insurable due to fire hazard risks. Faulty wires cause nearly 90 percent of residential fires, so this is something insurance companies take very seriously. If your home is found uninsurable due to wiring issues, it is vital to budget for necessary upgrades. If you don’t, your risk of fire is significantly amplified.

2) HVAC (Heating, Ventilation, and Air Conditioning): Does your home have central heating and air conditioning? What condition are the units in? Are there any signs of obvious damage such as leakage? Remember each insurance agency determines what it considers “acceptable” when insuring older homes; however, it’s not uncommon to see coverage denied for lack of central air and heat.

3) Plumbing: Inspectors at the type of pipes in your home to determine how likely they are to burst. If polybutylene plumbing is found coverage can be denied as these are more prone to bursting. However, some insurance companies may still insure you, but will exclude water damage. In that scenario, if there is a flood due to pipes bursting, you are 100 percent responsible for the total expense.

4) Roof: Roof age, material, and condition are what inspectors look for. Generally, insurance companies do not insure shingle roofs more than 20 years old or tile or metal roofs more than 40 years old. However, if your roof is younger but has apparent damage outside or water leaks inside your home, that might be cause to deny coverage.